Features

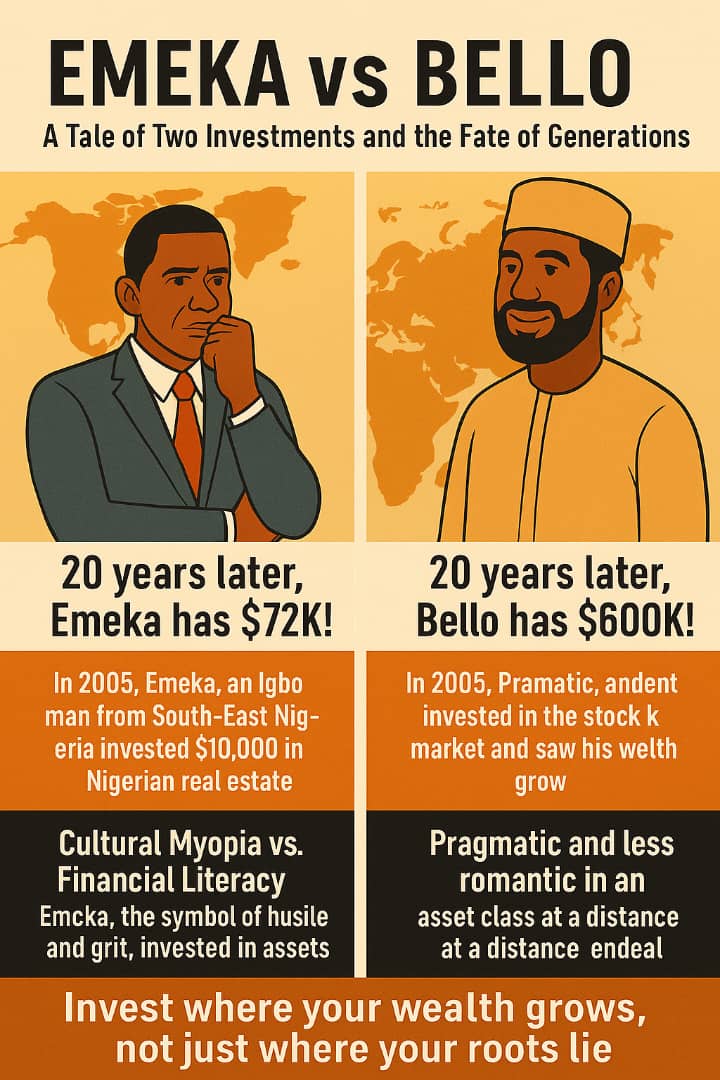

A Tale of Two Investments and the Fate of Generations

By Clara Innocent

In 2005, two Nigerian men stood at the precipice of a financial decision that would alter the trajectory of their lives and the legacy of their families.

Emeka, an industrious Igbo man from South-East Nigeria, had just completed a gruelling ten-year hustle in Atlanta, Georgia.

Through sheer determination, he had saved up $60,000 and secured a $40,000 low-interest loan, bringing his capital to a total of $100,000 USD. His dream? To invest in his homeland. Like many of his kin, Emeka believed that Nigerian real estate was the golden ticket to wealth.

Meanwhile, Bello, a shrewd politician and power broker from Northern Nigeria, didn’t toil abroad. Instead, he “sourced” converted ₦13.2m naira through his political networks and quickly converted it to hard currency, the equivalent $100,000 at the time, wisely aware of the naira’s instability.

But unlike Emeka, Bello wasn’t interested in the illusion of wealth. He wanted real capital preservation and growth.

The Diverging Paths

In early 2005, Emeka landed in Lagos and immediately purchased two plots of land in Lagos and Anambra, pouring his full $100,000 into what was then considered a prime investment. He returned to Atlanta, proud of his real estate empire, convinced he had outsmarted the American system.

Bello, on the other hand, wired his $100,000 (approx. ₦13.2m at the time) to a financial adviser in London. With 25% down, he secured a modest mortgage on a London flat and used the remainder as a deposit on a condo in Mississauga, Canada.

Between the two properties, he controlled over $400,000 worth of real estate using his $100,000 as equity — a classic leverage play.

Two Decades Later: The Reality Check

By 2025, Emeka’s two Nigerian plots of land, had appreciated to a massive ₦150 million. It looked very impressive on paper. But the naira had since collapsed from around ₦132 per 1$ to over ₦1,550 per $1. His investment, once worth $100,000, now converted to about $97,000 USD again — or even less, once inflation and transaction costs were considered.

Worse, property liquidity was low, and rents in Nigeria were mostly paid late or in cash, barely keeping up with the country’s 20%+ annual inflation. Emeka had not gained. He had merely preserved nominal value, while eroding global purchasing power.

Emeka has also had to repay some of the loans to his American bank at 12% per annum, meaning he had lost an additional $24,000 depreciating his net worth to $72,000 after 20 years of investment- A gross failure.

Meanwhile, Bello’s London and Mississauga properties had appreciated by 80% and 100% respectively in real terms. But more importantly, his rental income, denominated in GBP and CAD, had compounded over 20 years, covering his mortgage repayments and growing his equity.

His properties were now worth over $800,000 combined, with nearly $600,000 which in 2025 is ₦930m in net equity. His initial $100,000 had multiplied six fold — in hard currency. Even without leverage he would have had nearly ₦300m. So now Emeka has $72K and Bello $600K.

Cultural Myopia vs. Financial Literacy

20 years later Emeka has $72K and Bello has $600K! Emeka’s story isn’t unique.

Across Nigeria’s south-eastern region, generations of Igbo businessmen and returnees have poured money into land and buildings uncompleted mansions in ancestral villages, unoccupied flats in Enugu, and Lagos lands with no title documents.

Yet the cold truth remains: Nigeria’s currency and inflation have devoured these investments, leaving behind only a mirage of wealth.

Meanwhile, men like Bello less romantic, more pragmatic — continue to quietly convert naira to dollar and park wealth in stable markets.

While Emeka battles tenants, local land disputes, and currency shocks, Bello collects stable rent in pounds and Canadian dollars, reinvests his earnings, and watches as compound interest and currency stability propel his wealth skyward.

The Tragic Irony

The great irony is this: Emeka, the symbol of hustle, patriotism, and grassroots ambition, ends up eroding his financial destiny in a bid to honour his homeland. Bello, often derided for his political connections and flamboyant lifestyle, ends up preserving and growing family wealth across borders. One’s children inherit troubled deeds and falling assets, the other’s children inherit stable foreign assets and expanding global options.

The Lesson for a Generation

It is time for young Nigerian professionals — especially those abroad — to confront this hard truth. Investing in Nigerian property without accounting for inflation, currency risk, and systemic inefficiencies is not wealth-building. It’s wealth erosion disguised as asset growth.

Leverage, stable currencies, structured legal systems, and access to mortgage financing in places like London and Toronto make those markets not just profitable, but predictable and protective.

Emeka and his generations are not losing in the long-term because he lacked ambition. He and his people are literally bleeding generational wealth because they mistake “physical structures in their home country” as motion and progress.

But what they are doing in the long-term is carrying the losses that accrue through corruption accumulated by others. They ‘pump’ dollars and euros into Nigeria, while the corrupt politicians siphon dollars away to safer investments overseas.

Are certain peoples sustaining Nigeria from the brink, while others squeezing the resources for their own generation’s benefit?

If today the Emekas want to safeguard tomorrow’s legacies, they must learn from the Bellos of the world: “Invest where your wealth grows, not just where your roots lie.”

“Invest where your wealth grows, not just where your roots lie. ”-the Journey